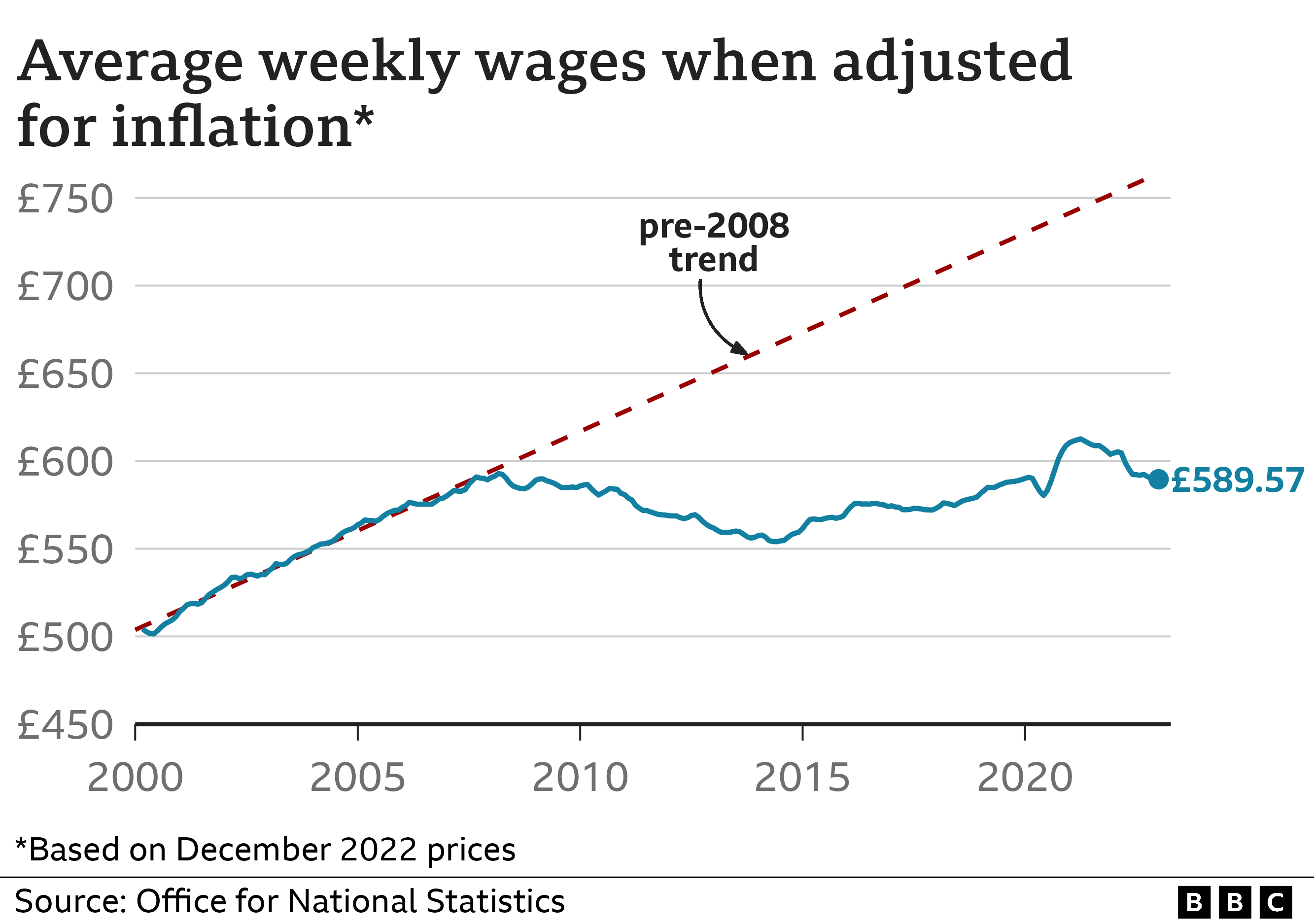

Europe’s industrial engine isn't just sputtering. It’s stalling in ways that make the dream of a quick 2026 recovery look like wishful thinking. While the latest data from January shows a contraction in Euro zone manufacturing, the real story isn't just about a single month of bad numbers. It’s about a structural breakdown. High energy costs aren't a temporary spike anymore. They’re a permanent tax on European competitiveness, and the factory floors from Stuttgart to Milan are feeling the squeeze.

If you’ve been following the European Central Bank (ECB) or reading the optimistic projections from late last year, you were told that falling inflation would spark a rebound. That hasn't happened. Instead, the Purchasing Managers' Index (PMI) for the manufacturing sector remained stuck below the 50-point mark that separates growth from contraction. It’s been under that line for over a year and a half. That isn't a "dip." It’s a trend that’s hollowing out the continent’s economic core.

The January figures are particularly stinging because they arrived just as global trade was supposed to stabilize. Instead, German industrial production—the supposed "locomotive" of Europe—led the decline. When Germany catches a cold, the rest of the Euro zone gets pneumonia. But this time, it feels like the flu has turned into something much more chronic.

The Energy Trap No One Wants to Talk About

Energy prices have dropped from their insane 2022 peaks, sure. But "lower" doesn't mean "competitive." European manufacturers are still paying significantly more for electricity and natural gas than their counterparts in the United States or China. I’ve talked to mid-sized factory owners in Northern Italy who say their margins are being eaten alive. They can’t just pass those costs onto consumers forever. Eventually, the buyers walk away.

This creates a vicious cycle. Because energy is expensive, companies cut back on investment. Because they don’t invest, their machinery gets older and less efficient. This makes them even more sensitive to energy prices. It’s a death spiral. Look at the chemicals and primary metals sectors. These are the building blocks of an economy. In January, these energy-intensive industries saw some of the sharpest drops in output. You can’t build a high-tech future if you can’t afford to make the basic materials.

The reality is that Europe’s "green transition" is hitting a wall of high costs. While the long-term goal is noble, the short-term execution is punishing the very industries that need to fund that transition. We’re seeing a massive shift where companies are quietly moving production to places like South Carolina or Vietnam. Once those jobs leave, they don’t come back.

Why Interest Rate Cuts Might Not Save the Day

Everyone is waiting for the ECB to slash rates. The logic is simple: cheaper money equals more borrowing, which equals more growth. But that assumes the problem is a lack of liquidity. It isn't. The problem is a lack of demand.

European consumers are nervous. They’re sitting on savings because they don't know if their jobs will exist in two years. In January, new orders for manufactured goods fell again. If nobody is buying, it doesn't matter if a loan costs 3% or 5%. A factory owner isn't going to buy a new production line if the warehouse is already full of unsold inventory.

- The Inventory Glut: Companies over-ordered during the supply chain chaos of 2022 and 2023. Now they’re "destocking."

- The China Factor: China isn't just a buyer of German cars anymore; they’re a fierce competitor in the EV space.

- Geopolitical Friction: Red Sea shipping disruptions are adding "stealth inflation" back into the system, making parts more expensive and slower to arrive.

Basically, the ECB is in a corner. If they cut rates too fast, they risk reigniting inflation. If they wait too long, they watch the industrial base crumble. Most analysts expect a cautious approach, but "cautious" won't fix a factory that’s already decided to relocate to North America.

Germany is No Longer the Savior

For decades, the Euro zone relied on Germany to pull everyone else out of a hole. That's over. Germany’s business model—cheap Russian gas plus high-end exports to China—is broken. The gas is gone, and China is now building its own high-end machines.

In January, German industrial output fell by more than the consensus estimate. This dragged down the entire bloc's performance. The French and Spanish industrial sectors showed a bit more resilience, but they can't carry the weight of a struggling Germany. We’re looking at a multi-speed Europe where the biggest engine is the one that's smoking.

I’ve seen plenty of "rebound" headlines over the last six months. They usually focus on the services sector—tourism, dining out, and software. And while services are great, you can't run a world-class economy on lattes and apps alone. Industry provides the high-paying, stable jobs that support the rest of the economy. When manufacturing shrinks, the middle class shrinks with it.

The Reality of Deindustrialization

This isn't just a "bad patch." It’s the sound of deindustrialization. When you look at the January data, pay attention to the "output expectations" component. It’s dismal. Managers aren't just worried about today; they’ve lost faith in tomorrow.

The cost of capital is high, labor shortages are persistent despite the slowdown, and the regulatory burden in the EU is becoming a nightmare for smaller firms. It’s a "death by a thousand cuts" scenario. The Euro zone needs more than just a rate cut. It needs a massive overhaul of its energy policy and a serious reduction in the red tape that makes it impossible for a startup to build a factory.

Stop looking for a "V-shaped" recovery. It’s not coming. We’re likely looking at an "L-shaped" stagnation for the industrial sector throughout the rest of 2026. The companies that survive will be the ones that pivot fastest to automation and localized supply chains.

If you’re managing a portfolio or running a business that relies on European trade, stop waiting for the "good old days" to return. They aren't. Diversify your supply chain away from the most energy-dependent regions of Central Europe. Focus on sectors with high intellectual property value rather than high energy intensity. Watch the 10-year bund yields closer than the ECB press releases. The market is already pricing in a much slower, much grittier reality than the politicians are willing to admit. The January slump was a warning. Ignore it at your own peril.